NCERT Solutions for Class 12 Entrepreneurship Chapter-5 Business Arithmetic

TEXTBOOK QUESTIONS SOLVED

A. VERY SHORT ANSWER TYPE QUESTIONS

Question 1. Explain the following terms with proper example:

- SKU

- Cash flow

- Cash inflow

- Cash outflow

- Re-order point

- Cash flow projection

- Cash conversion cycle

Answer.

- SKU: Stock Keeping Unit (SKU) code

(a) All items in the inventory is to be identified with a unique code which signifies certain aspects of the item.

(b) It can be colour, size, weight or any other characteristics that is of importance in its use.

(c) The SKU code can be a combination of alpha and numeric.

(d) SKU is the very basic unit for data collection and further manipulation for deriving meaningful statistics and decision making.

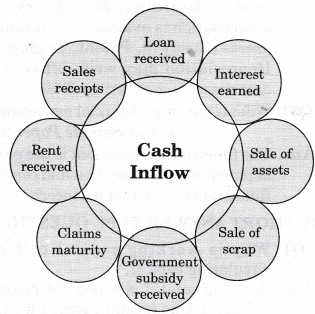

(e) Bar Codes and RFID (Radio Frequency Identification tags are used in tracking etc. using SKU. - Cash flow: Cash flow refers to the movement of money in and out of a business during a specific period of time.

Example: Loan Received, Sales Receipts, Sale of Assets. - Cash inflow: All receipts of money in the business is known as cash inflow like rent received and loan received.

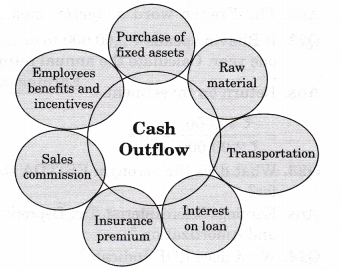

- Cash outflow: It is defined as the movement of money out of a business.

Example: Furniture and Fixtures, Interior Decoration, Tools, Computers, Raw Material.

(a) Re-order point: It is a level at which a new order must be placed so that the inventory is renewed before the stock reaches zero level.

It is estimated by using the formula Reorder Point = Usage Rate x Lead Time. - Cash flow projection: Cash flow projection shows how cash is expected to flow in and out of your business.

- Cash conversion cycle: (CCC or Operating Cycle) is the length of time between a firm’s purchase of inventory and the receipt of cash from accounts receivable. It is the time required for a business to turn purchases into cash receipts from customers.

CCC represents the number of days a firm’s cash remains tied up within the operations of the business.

Question 2. Pareto’s Law formed the basis for a technique. Name it.

Answer. The principle is named for Vilfredo Pareto, an Italian economist who studied land ownership in Italy in the early 1900’s and found that roughly 20 per cent of the population held title to about

80 per cent of the land. Pareto’s law has applications throughout science as well as business, including inventory control, where it forms the basis for a technique called ABC analysis.

B. SHORT ANSWER TYPE QUESTIONS-I

Question 1. What is ABC analysis?

Answer.ABC analysis is an inventory categorization method which consists in dividing items into three categories (A, B, C):

- A being the most valuable items.

- B-items are the inter class items, with a medium consumption value.

- C being the least valuable ones.

This method aims to draw managers’ attention on the critical few (A-items) not on the trivial many (C-items).

Question 2. What is Pareto’s Principle?

Answer. In 1906, Italian economist Vilfredo Pareto noted that 80% of Italy’s land was owned by 20% of the people. Pareto principle is a prediction that 80% of effects come from 20% of causes. The 80:20 ratio of cause-to-effect became known as the Pareto Principle. He became somewhat obsessed with this ratio, seeing it in everything. For example, he observed that 80% of the peas in his garden came from 20% of his pea plants.

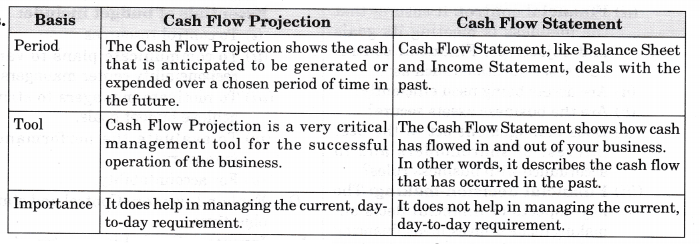

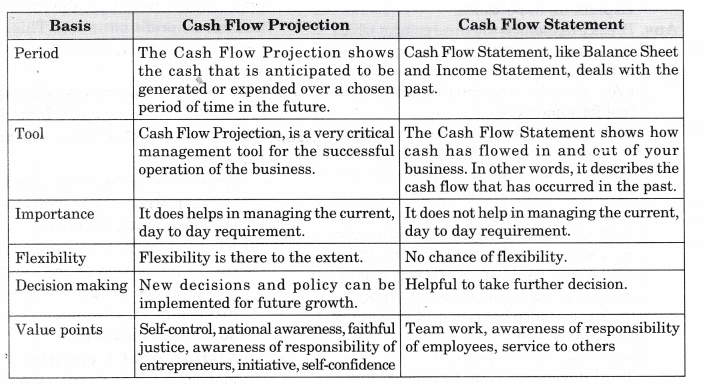

Question 3. Differentiate between cash flow projection and cash flow statement.

Answer.

Question 4. What is financial management? What is the main objective of financial management?

Answer.

- Financial management means planning, organizing, directing and controlling the financial activities such as procurement and utilization of funds of the enterprise.

- It is an activity which is concerned with acquisition and conservation of capital funds in meeting financial need an overall objectives of business organisation.

- It means applying general management principles to financial resources of the enterprise.

The main objectives of financial management is wealth maximization of shareholder’s wealth.

- To ensure regular and adequate supply of funds to the concern.

- To ensure adequate returns to the shareholders.

- To ensure optimum funds utilization. Once the funds are procured, they should be utilized in maximum possible way at least cost.

C. SHORT ANSWER TYPE QUESTIONS-II

Question 1. There are three key elements in the process of financial management. Explain them.

Answer.

- Financial planning: Management need to ensure that enough funding is available at the right time to meet the needs of the business.

(а) The short term funding may be needed to invest in equipment and stocks, pay employees and fund sales made on credit.

(b) The medium and long term funding may be required for significant additions to the productive capacity of the business or to make acquisitions. - Financial control: It ensures that the business is meeting its goals and objectives. Financial control addresses questions such as:

(a) Are assets being used efficiently?

(b) Are the business assets secure?

(c) Does management act in the best interest of shareholders and in accordance with business rules? - Financial decision-making: The key aspects of financial decision-making relate to investment, financing and dividends. For example, it is possible to raise finance from selling new shares, borrowing from banks or taking credit from suppliers.

(a) A key financing decision is whether profits earned by the business should be retained or distributed to share¬holders through dividends.

(b) If dividends are too high, the business may be starved of funding to reinvest in growing revenues and profits further.

Question 2. What are the key aspects of financial decision-making?

Answer. The key aspects of financial decision-making relate to investment, financing and dividends. Investments must be financed in some way however there are always financing alternatives that can be considered.

For example, it is possible to raise finance from selling new shares, borrowing from banks or taking credit from suppliers:

- A key financing decision is whether profits earned by the business should be retained rather than distributed to shareholders via dividends.

- If dividends are too high, the business may be starved of funding to reinvest in growing revenues and profits further.

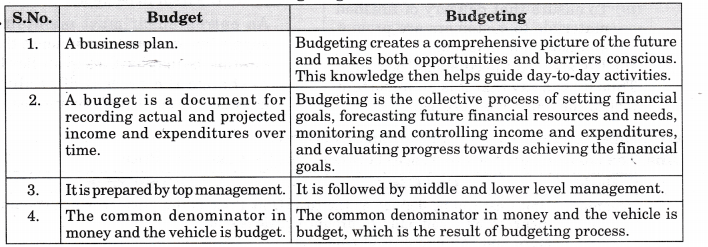

Question 3. What is a budget? What are the essentials of a budget?

Answer. For any business, a budget is a quantitative expression of a plan for a defined period of time. It may include planned sales volumes and revenues, resource quantities, costs and expenses, etc. Essentials of budget include:

- To control resources

- To communicate plans to various responsibility center managers.

- To motivate managers to strive to achieve budget goals.

- To evaluate the performance of managers.

- For accountability.

Question 4. Explain Inventory Control and state its objectives.

Answer. Inventory Control is a systematic and detail record of purchase of materials, their storage capacity, quantity in order to supply quantity order for large discounts, handling delivery of materials etc. It is a process which facilitates an entrepreneur in smooth production operation and to take important decisions in a production line.

The objectives of inventory management are:

- To ensure that the supply of raw materials and finished goods will remain continuous so that production process is not halted and demands of customers are duly met.

- To minimise carrying cost of inventory.

- To keep investment in inventory at optimum level.

- To reduce the losses of theft, obsolescence and wastage, etc.

(a) To make arrangement for sale of slow moving items. - To minimise inventory ordering costs.

D. LONG ANSWER TYPE QUESTIONS

Question 1. What is a budgeting process?

Answer.

- Budgeting is a collective process in which operating units prepare their plans in conformity with corporate goals published by top management.

- Each unit plan is intended to contribute to the achievement of the corporate goals.

- Unit managers prepare projections of sales, operating costs, overhead costs, and capital requirements. They calculate operating profits and returns on the investment they intend to use.

The budget itself is the projection of these values for the next calendar or fiscal year.

In this process, each unit presents its plans and budget to a reviewing upper management panel and may, thereafter, make whatever changes result from instructions or negotiations with the higher level.

Texts presenting, documenting, and defending the rationales underlying the numbers are usually part of the planning document.

Approved budgets then become the road¬map for operations in the coming year. Ideally monthly or quarterly budget reviews track performance against the budget.

As part of such reviews, changes to the budget may be approved. At the end of year managers are judged by their performance against the budget.

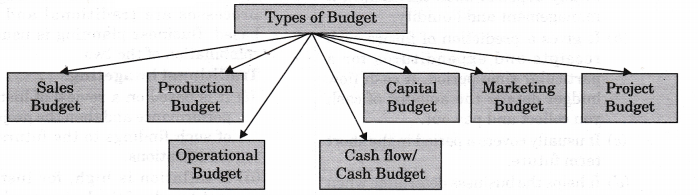

Question 2. There is a Budget to suit every business and its need. Elucidate.

Answer.

- Sales Budget:

(a) This budget shows what finished products can be sold in what quantities and at what prices.(an estimate of future sales)

(b) It may be prepared product wise, region wise, customer wise and period wise.

(c) It is often broken down into both units and currency. - Production Budget: It is always based on sales budget. It is generally prepared into two parts:

(a) It shows the estimates in volume or quantities. It estimates the number of units that must be manufactured to meet the sales goals.

(b) It shows production cost. The production budget also estimates

the various costs involved with manufacturing those units, including labour and material, - Capital Budget:

(a) It is generally prepared to estimate the total capital required for acquiring the fixed assets for fulfilling the production demand of an organisation.

(b) Long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth pursuing. Capital required for developing research and development should be totally different from the work of manufacturing unit.

(c) The capital budget helps you figure out how much money you need to put in place of new equipment or procedures to launch new products or increase production or services.

(d) This budget estimates the value of capital purchases you need for your business to grow and increase revenues. - Cash Flow/Cash Budget/Financial Budget:

(a) It is one of the important budgets because success of any business totally depends upon the cash flow management and liquidity.

(b) It gives a prediction of future cash receipts and expenditures for a particular time period. A cash flow budget details the amount of cash you collect and pay out.

(c) It usually covers a period in the short term future.

(d) It helps the business determine when income will be sufficient to cover expenses and when the company will need to seek outside financing.

(e) It makes a provision for minimum cash balance which will be available at all times.

(f) The minimum cash balance should be equal to one month’s operating expenses including contingencies.

(g) A positive cash flow is essential to grow your business. - Marketing Budget: It is an estimate of the funds needed for promotion, advertising, and public relations in order to market the product or service.

- Project Budget:

(а) It estimates of the costs associated with a particular company project. These costs include labour, materials, and other related expenses.

(b) The project budget is often broken down into specific tasks, with task budgets assigned to each. A cost estimate is used to establish a project budget. - Operational Budget:

(a) An operational budget is the most common type of budget used.

(b) It forecasts and tries to closely predict yearly revenue and expenses for a business.

(c) It is a short term budget.

(d) This budget can be updated with actual figures on a monthly basis and then you can revise your figures for the year, if needed.

Question 3. Explain the two dominant forms of budgeting process.

Ans. The two dominant forms of budgeting processes are traditional and zero- based. Business planning is usually a combination of the two.

Traditional budgeting:

- It is based on a review of historical performance and then the projection of such findings to the future with modifications.

- If inflation is high, for instance, cost trends of the last several years are projected forward but with adjustments both for inflation and for projected growth or decline in business activity.

- Historical sales patterns, using established trends in sales growth, are projected; new sales from planned new product introductions are then added.

Zero-based budgeting:

- It is the creation of a completely new budget from the ground up—as if no history existed.

- When using this method, the operation must justify and document every item of expenditure and income anew.

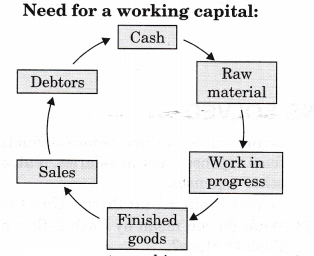

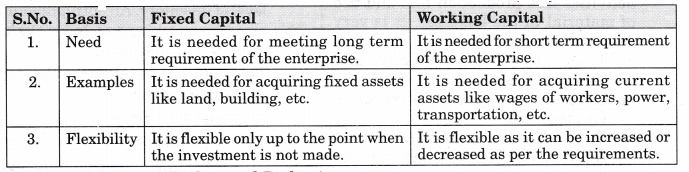

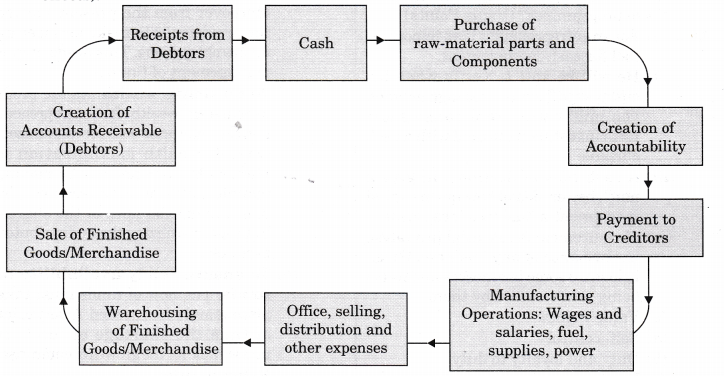

Question 4. What is working capital? What is the need for a working capital?

Answer.Money needed to fund the normal, day- to-day operations of a business is known as the working capital.

- Adequate working capital is required for the smooth running of any business.

- It is required by a business for meeting day to day business expenses to complete a business cycle or the operating cycle.

The working capital of a business keeps on circulating or changing since the money circulates in various forms of assets in a continued manner.

The above diagram explains that:

- In a business concern operating cycle begins with outflow of cash towards the purchase of raw materials, payment of labour, power, fuel and other expenses converting the raw materials into work in progress and converting them into finished goods. Sale of finished good for cash or credit.

- If on credit then conversion of account receivables into cash.

- This operating cycle indicates that funds once tied up in the form of raw materials are later converted into the form of finished goods.

- In a manufacturing concern there is a time gap between the first step of purchasing of raw-materials to last step of selling of goods and realizing cash. This time duration is called operating cycle. It is also called the “changing” or circulating capital because money circulates in various forms of assets in a continued manner.

E. HIGHER ORDER THINKING SKILLS (HOTS)

Question 1. Calculate working capital of Raja & Co. has the following items in its Balance sheet: Stock — 50,000; Trade creditors – 32,000; Debtors – 75000; Cash -1,00000; Dividend payable – 50,000; Tax – 44,000; Short term loan – 61,000; Short term investments – 76,000. Calculate gross and net working capital.

Answer.

- Total Current Assets = Debtors + Stock + Cash + Short term investment Total Current Assets = (Rs 75000 + Rs 50,000 + Rs 1,00000 + Rs 76,000) Total Current Assets = Rs 3,01,000

- Total Current Liabilities = Sundry Creditors + Dividend Payable + Tax + Short Term loan)

Total Current Liabilities = (Rs 32,000 + Rs 50,000 + Rs 44,000 + Rs 61,000) = Rs 1,87,000 - Gross Working Capital = Total Current Assets

Gross Working Capital = Total Current Assets = Rs 3,01,000 - Net Working Capital = Total Current

Assets – Total Current Liabilities

Net Working Assets = Rs 3,01,000 – Rs 1,87,000 = Rs 1,14,000

(a) Gross Working Capital = Rs 3,01,000

(b) Net Working Assets = Rs 1,14,000

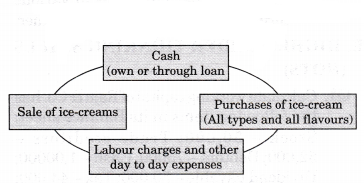

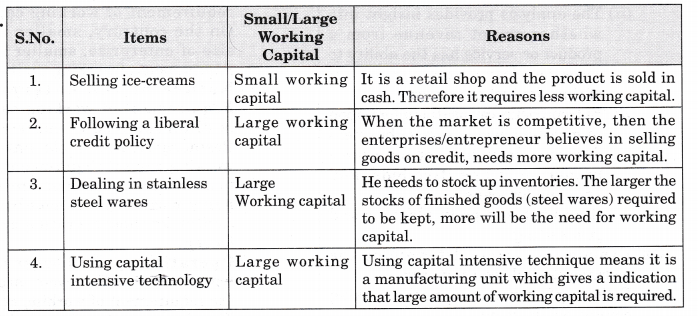

Question 2. Ramu is buying and selling ice-cream.Explain his working capital requirement.

Answer. Ramu is a trading entrepreneur.

- Trading entrepreneur is one who undertake trading activities, whether domestic or overseas.

- They deal in buying and selling of manufactured goods.

- Before launching the business they identify the potential market for his product in order to stimulate the demand.

They believe in creating a demand in the market to market survey and push many ideas ahead of others in the form of demonstration to promote

Operating cycle or cash conversion cycle for trading business:

- Money needed to fund the normal, day to day operations of a business is known as the Working Capital.

- For trading, where there is no manufacturing (or conversion), the operating cycle will be shorter.

- Ramu needs less amount of working capital as ice-cream is a perishable goods and can’t keep for a long time period.

- Therefore, Ramu has to purchase and sale of goods through cash only.

MORE QUESTIONS SOLVED

I. VERY SHORT ANSWER TYPE QUESTIONS

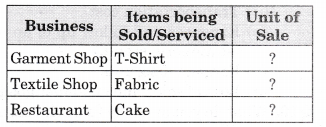

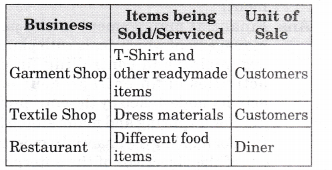

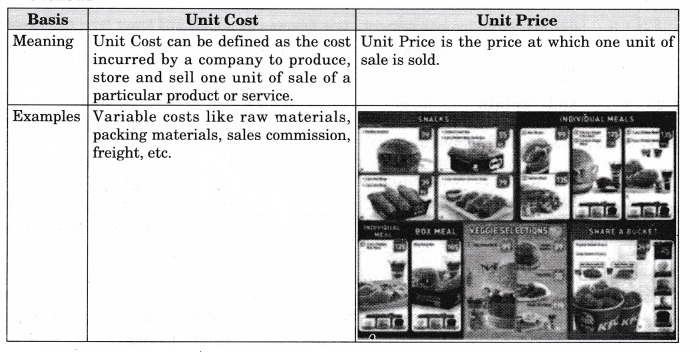

Question 1. What do you mean by Unit of Sales?

Answer. Unit of sales can be defined as the measure of what products are sold.

Question 2. What do you mean by Gross Profit?

Answer.Excess of Unit Price over Unit Cost is known as the Unit Gross Profit or Unit Gross Margin. This represents the business’s profit from selling a product

or providing service before deducting fixed expenses such as salaries, rent, and other expenses.

Gross Profit = Unit Price — Unit Cost

Question 3. What do you mean by Cash Inflow and Cash Outflow?

Answer. All receipts of money is known as cash in flow 5 like rent received and loan received, and payments made in money is known as cash outflow. Ex: Insurance premium and Transprtation charges.

Question 4. Give one difference between Income Statement and Cash Flow Statement.

Answer.

Question 5. What do you understand by Unit Cost/ Variable Cost/Cost of Goods sold?

Answer. Cost of unit can be defined as the cost incurred by a company to produce, store and sell one unit of sale of a particular product or service.

Question 6. Give some examples of Variable Cost/ Unit Cost.

Answer. The Unit Cost refers to the variable cost like raw-materials, packing material, sales commission, freight, etc.

Question 7. How do we calculate the unit cost in the case of multi product or service situations? Explain with the help of an example.

Answer. Grocery store is a trading business. One buys and sells. So, the cost at which the items are purchased is known as Unit Cost (just as its MRP at which you are selling). Therefore, at the end of the day, it is possible to know the purchase price of all the items and quantities that were sold. Let us suppose that it works out to Rs 1,70,000. There are 100 units of Sale. So the unit cost is Rs 1,700.

Question 8. What is MRP?

Answer. MRP is a short form of Maximum Retail Price. It is a price at which shopkeeper sells the goods to customers.

Question 9. What are “Carrying Costs”?

Answer. It is defined as the cost of holding and handling materials inside or outside the stores. It is important to examine the inventory level and to maintain optimum balance of inventory.

Question 10. What do you mean by Order lead time?

Answer. It is an average time that elapses between placing an order and receiving the goods.

Question 11. What do you understand by Usage Rate?

Answer. It is an average rate at which the inventory is drawn down over a period.

Question 12. How Cash Flow Projection will be considered as a better idea for your business plan?

Answer. As part of a business plan, Cash Flow Projection will always give an entrepreneur a much better idea, of how much capital investment a business idea needs to start and to run the business.

Question 13. Give four examples of inflow of cash in the business.

Answer.

Question 14. Define Budget.

Answer. ICMA London defines a budget as “financial and quantitative statement, prepared and approved prior to a defined period of time, of the policy to be persued during that period for the purpose of attaining a given objective.” It may include income, expenditure and capital.

Question 15. Give a few examples of Outflow of cash in the business.

Answer.

Question 16.What are the key aspects of financial decision-making?

Answer. The key aspects of financial decision-making relate to investment, financing and dividends.

Question 17. Give some examples of current assets.

Answer.

- Cash and bank balances

- Account receivables:

(a) Bills receivable, and

(b) Debtors - Short term investments/Temporary investment

- Prepayment:

(a) Prepaid rent,

(b) Unexpired insurance, etc. - Accrued Income

Question 18. Give some examples of Current Liabilities.

Answer.

- Bank overdrafts

- Accounts Payable: (a) Creditors (b) Bills payable

- Outstanding Expenses: wages, rent, commission, etc.

- Income received in advance

- Dividend Payable

- Provision for doubtful debt.

Question 19. What is the desirable behaviour of any inventory item?

Answer.Desirable behaviour of any inventory item is “Availability”. It means that there should never be any stock out.

In other words, moment the need (demand) arises we should be able to supply the item- without losing any time.

Question 20. Name the French word for the origin of the word ‘Budget’.

Or

Write the etymology of the word “Budget”.

Answer.The French word bougette, meaning purse (referring to money), is the origin of the word budget.

Question 21. What do you understand by Budget Period?

Answer. It refers to the period for which a budget is prepared and implemented.

Question 22. If Bhavin spends Rs 2,00,000 to open a grocery shop and earns a net profit of Rs 40,000 in one year. Calculate the annual return on investment.

Answer.

Question 23. What does the acronym EBITDA stand for?

Answer. Earnings Before Interest, Tax, Depreciation and Amortization.

Question 24. What does ROE Indicate?

Answer. ROE (Return On Equity) is a good indicator to know a true measure of how own money is being used.

Question 25. What does ROI Indicate?

Answer. ROI (Return On Investment) is a good indicator to know a true measure of how total money is being used. ROI, on the other hand, gives an indication of how the total money is being used.

Question 26. Give one example each of bulky items with low value and high value items with low volume.

Answer.

- Bulky items with low value – straw for use in paper mill.

- High value items with low volume — Diamond.

Question 27. Give four examples of items which are hazardous in nature and special precautions have to be taken in their storage.

Answer. Gasoline, other combustible items, some hazardous chemicals, etc.

Question 28. Give four examples of items are hazardous in nature and special precautions have to be taken in their manufacturing.

Answer. In a factory manufacturing safety matches, phosphorous and potassium chlorate are not stored in the same or even adjoining areas, for fear of accidental mix up.

Question 29. What do you mean by shelf-life? Give two examples.

Answer. The length of time a product may be stored without becoming unsuitable for use or consumption. Items like vegetables, fruits, flowers and fish are perishable in nature. This calls for special storage conditions and equipments – cold storage, freezers, etc. These have financial implications. Similarly some of the manufactured food or medicinal products have expiry dates – beyond which they are not fit for consumption. This imposes certain constraints on inventory management.

Question 30. Give one difference between amortisation and depreciation.

Answer. Depreciation is applicable for tangible assets (Building, Machinery) and amortisation is available for intangible assets (Goodwill, Patent, Trademark). Depreciation may write off slow but amortisation may write off fast.

Question 31. What is meant by ‘financial management’?[CBSE Sample Paper 2016]

Answer. Financial management is the process of procurement, allocation and control of financial resources of a concern.

II. SHORT ANSWER TYPE QUESTIONS

Question 1. Why is working capital called as circulating capital?

Answer. Working capital is called the changing or “circulating capital”, since the money circulates in various forms of current assets in a continued manner.

For example: Funds once tied up in the form of raw materials are later converted into the form of finished goods which are not ultimately sold.

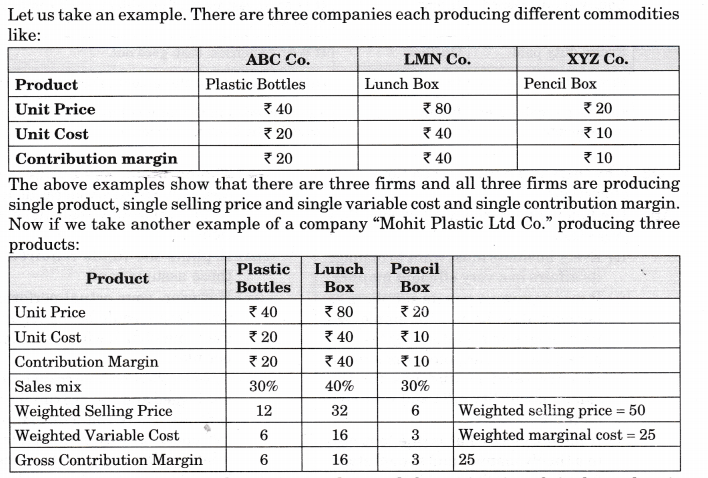

Question 2. Write down the formula for calculating the weighted-average contribution margin per unit for the sales mix.

Answer. Suppose a manufacturing unit produces three products A, B, and C. Then the following formula is used:

Product A CM (contribution mix) per unit x Product a sales mix percentage + Product B CM per unit x Product B sales mix percentage + Product C CM per unit x Product C sales mix percentage = Weighted average unit contribution margin

Question 3. Give some examples of Carrying Cost.

Answer. Examples of Carrying Cost are:

- Money tied up in inventory

- Storage on inventories

- Taxes on inventories

- Obsolescence cost

(a) Handling and transfer - Deterioration of quality

- Cost of maintaining inventory records.

Question 4. What is an Inventory?

Answer. Inventory means detailed list of items used in the business. It refers to stock of goods in the form of raw materials, work in progress and finished goods, a firm can make up the product and kept for sale in ordinary course of business. Thus, inventories make a linkage between production and sale of goods.

Question 5. When an entrepreneur’s business is expanding, his business outflows can be more than his business inflows. Do you agree. How?

Answer. Yes, when an entrepreneur’s business is expanding, his business outflows can be more than his business inflows. It is so because there is always a lag between your spending (on raw materials, labour, etc.) and receiving the sales revenue. Receipt of sales revenue may be delayed because he might have given credit or you have produced ahead of the sales (to cater to the high demand during festive season) and are temporarily holding finished goods stock.

Question 6. Write Unit of Sale in each case.

Answer.

Question 7. What do you mean by Reorder Point? How it is calculated?

Answer. It is a level at which a new order must be placed so that the inventory is renewed before the stock reaches zero level. It is estimated by using the formula: Reorder Point = Usage Rate x Lead Time

Example: Suppose a company uses 15 units of an item per day (usage rate, and the order lead time is 10 days, a new order must be placed when the inventory level reaches 150 units (Reorder Point 150 = Usage Rate 15 x Lead Time 10) so that inventory is replenished before a stock out occurs.

Question 8. Why financial control is considered as an important activity?

Answer. Financial control is a critically important activity to help the business ensure that the business is meeting its objectives.

It also addresses following points like:

- Efficient usage of all business assets

- Security of all business assets.

- Taking interest of all shareholders of the company and going in accordance with business rules.

Question 9. What are Order Processing Costs?

Answer. The cost is associated with the placement of an order for the acquisition of inventories. It is determined on the basis of expenses incurred in the purchase department. Some of the components of cost are:

- Finding the sources of supply

- Obtaining quotations

- Transportation cost

- Expenses and follow up of an order (stationery, stamp)

- Forgone discounts

- Loss of sales and customer goodwill.

Question 10. What do you mean by financial management?

Answer. Financial management is the part of management which deals with planning, organizing and controlling financial activities of an entrepreneur or the activity undertaken by the entrepreneur,

- For acquiring and maintaining fund.

- For fulfilling the financial requirements of the objectives of the enterprise.

- And for attaining the goals and objectives of the enterprise.

Question 11. “The Budget period for all the business are same”. Do you agree? Comment. Answer. No, I don’t agree with the statement. The budget period will depend upon the type and size of business enterprise and control aspect.

- For seasonal enterprise (food and clothing) short period generally should cover one season.

- For heavy industries with heavy capital expenditure (heavy engineering works/automobile industries) the budget period is generally long.

Question 12. What are the assumptions to be made for sales mix, for the calculation of break even point?

Answer. Following assumptions are made:

- The proportion of sales mix must be predetermined.

- The sales mix must not change within the relevant time period.

- All cost can be categorized as variable or fixed.

- Sales price per unit, variable cost per unit and total fixed cost are constant.

- All units produced are sold.

Question 13.Why is Return on Investment deemed as a yardstick for the performance of an enterprise?

Answer. Return on Investment is a relationship between profit before interest and tax and capital employed. It is deemed as a yardstick for the performance of an enterprise because it measures the overall profitability and efficiency of the enterprise in relationship to investment made by an entrepreneur in business. Higher the ratio, higher the overall profitability of the business. The ratio is compared with earlier years ratio and important conclusions are drawn from such comparison. As a yardstick it also shows how efficiently the resources are used in the business.

Question 14. What is B.E.P? Why an entrepreneur should know about it?

Answer. The business to break even when its value is equal to its total cost. The Break Even Point (B.E.P) is the sales volume at which there is neither profit nor loss, cost being equal to revenue. Break Even Point is a neutral point. Sales below this point show loss and sales excess of this point show profit. It is the relationship amongst cost of production, volume of production, profit and the sales value. The entrepreneur should know B.E.P as:

- He can forecast about profit accurately.

- He can ascertain costs, sales and profits at different levels of activity.

- For taking decision regarding price policy.

Question 15. Explain the various categories of inventory.

Answer. In a manufacturing firm inventories work as a link between production and sale. The three categories of inventories are as follows:

- Raw materials: Those materials which have purchased and stored in a godown at a particular time for future production.

- Work in progress: These are the goods in the course of manufacture. It means goods which are likely to be in various stages but not reached to the final stage. It consist of material, labour and factory expenses applied to the unit up to the last stage. In these the goods are in semi-finished stage.

- Finished goods: These are the goods reached at the final stage of production process. These goods are ready for sale. The size of three types of inventories depends upon varying nature of their business.

Question 16. Why is inventory control essential for an enterprise?

Answer. The process of inventory control gives direction to the entrepreneur to take important decision about the various activities like production line and use of material in the business. It is very essential for the enterprise:

- To ensure efficient, effective and optimum use of raw materials.

- To know the availability of resources for production.

- To ensure and make efforts to purchase raw materials in bulk to get quantity discounts.

- To ensure that delivery of finished materials to customers are prompt and not being delayed.

- To stabilize the fluctuation of demands. Thus we can say that it is an important tool in the hand of enterprise.

Question 17. What factors should be kept in mind for ordering an inventory?

Answer. Inventory means list of materials used in a business. An entrepreneur must be very careful and wise while deciding about the level of inventory. An entrepreneur must avoid overstocking and under-stocking of each item of the inventory.

The factors that influence the decision on such orders are:

- Order lead time

- Usage rate or rate of consumption

- Reorder-point or minimum quantity of the item to be kept.

An entrepreneur must maintain the supply line in a proper manner so that at any time he may have adequate flexibility to change the process of production according to customer’s requirement.

Question 18. Differentiate between Unit Cost and Unit Price.

Ans. The following are the differences between Unit Cost and Unit Price.

Question 19. What is the need of financial management?

Answer. Financial management is needed for:

- Ensuring availability of funds in the right amount at the right time.

- Ensuring the safety of funds.

- Ensuring efficient utilization of the available fund.

- Ensuring the desired level of income and profit.

Question 20. Explain trading on equity with the help of a suitable example.

Answer. Trading on equity relates to a situation when the debt component is likely to provide higher rate of return on share capital.

Debt and equity are the two sources of finances. Both have their own merits and demerits.But when a mix of both is used wisely, the rate of return equity can increase. This is because the interest paid on the loan is deductible from earning before tax payment. The payment of dividend is only made after realizing the interest.

Question 21. Distinguish between Fixed Capital and Working Capital.

Answer. The following are the differences between fixed capital and working capital.

Question 22. Distinguish between Budget and Budgeting.

Answer.

Question 23. Name and explain the chief cost of budget process.

Answer. The chief cost of the budget process is time. In some corporations the process takes on a life of its own and becomes a convoluted exercise of excessive complexity which, moreover, prevents unit managers from doing any thinking: their time is consumed in efforts to comply with a vast array of requirements dictated from above.

Much of the negative attitude that has developed concerning this activity has its roots in unnecessary bureaucratic impositions on the one hand and unreliability because of the rapid change, a few months out.

Question 24. What do you understand by sales mix? State the assumptions made for the calculation of break even point for sales mix.

Answer. Sales mix is the proportion in which two or more products are sold.

For the calculation of break even point for sales mix, following assumptions are made:

- The proportion of sales mix must be predetermined.

- The sales mix must not change within the relevant time period.

- All cost can be categorized as variable or fixed.

- Sales price per unit, variable cost per unit and total fixed cost are constant.

- All units produced are sold.

Question 25. Explain the concept of ROI (Return on Investment).

Answer. Meaning: It is the ratio of net profit before interest and tax and total investment. Significance: The significance of computing this ratio is to find out how efficiently the long term funds supplied by the outsiders or creditors and owners are being used.

It gives an indication of how the total money is being used.

Example: If an entrepreneur spends X 100,000 to open a grocery shop and makes a net profit of? 20,000 in one year, your annual ROI equals (20,000/100,000) x 100 = 20 per cent.

When calculating ROI, the investment will include not only what the investor spent out of his/her pocket, but also all borrowed funds.

Question 26. Explain the concept of ROE (Return on Equity).

Answer. Meaning: It is the ratio of net profit after interest and tax and owner’s investment. Significance: The significance of computing this ratio is to find out how efficiently the owners funds supplied by the shareholders/owners are being used. Example, if Sushmita the owner of a grocery shop has an equity stake of Rs 70,000 in the business, she has borrowed Rs 30,000 (rate of interest is 10%).

This will attract an interest of 3,000 @ 10% per annum.

If the Net Profit is Rs 14,000 then:

ROE=Rs 14,000/Rs 70,000 x 100 =20%

Question 27. Is ‘Break-even Analysis’ useful to achieve the target level of profit?

Answer. Yes, organisation’s identify those products, which yield the highest contribution. ‘Break even Analysis’ helps the firm in selecting and ranking those products, based on contribution, to achieve the targeted level of profit.

Question 28. Make a SKU form for “Shirts” for the given number, classify them in Style, colour, date, month, year, size: 01234- 021-R- Ma 31-10-40 M.

Answer. Style: 01234-021, Colour: R-Red, Month: Ma-May, Date: 31st, Year: 2010, Size: 40 Medium.

Question 29. Name the commonly used tags for tracking while using SKU.

Answer. Bar Codes and RFID (Radio Frequency Identification) tags are used in tracking containing electronically stored information.

Question 30. Name few different system of inventory control.

Answer.

- ABC Analysis

- Economic Order Quantity

- Just-in- time (JIT),

- Perpetual inventory, etc.

Question 31. What is RFID?

Answer. Radio-Frequency Identification (RFID) is the wireless use of electromagnetic fields to transfer data, for the purposes of automatically identifying and tracking tags attached to objects. The tags contain electronically stored information.

III. LONG ANSWER TYPE QUESTIONS

Question 1. What is the procedure to prepare a cash flow projection?

Or

How to develop a cash flow projection?

Or

What steps are to be taken to develop a cash flow projection?

Answer. Step 1: Every enterprise has different guidelines and rules and regulations. It is based on the business charateristics, decides on the frequency and period (day, week or month) as well as horizon (month, 13 weeks or 6 months).

Step 2: Develop the format, with items appropriate for your business, which will be used for developing the projection. You may take help from the formats attached here as sample.

Step 3: A projected cash flow begins with the existing cash balance for the business. It then lists the sources of inflow and the anticipated payment dates.

Step 4: For example, if you supply goods on credit, you will know at the start of February that you will receive a certain amount during the month covering sales from January – based on credit terms. You may have other inflows interest on your deposits, sale of scrap, rent from space sub-let etc. In this manner, you add up all your inflows.

Step 5: The statement then looks at forthcoming expenditure. Some of this will be a fixed, regular sum such as staff costs. Other expenses will be known but only payable at certain times, such as taxes. There will also be variable costs such as buying stock or materials.

Step 6: Where payment dates are variable, it is usually safest to work on the basis that you will pay suppliers as soon as possible but not receive payment from customers until the last possible date. Step 7: In short, be conservative in assumptions.

- Adding all outflows enables you arrive at the surplus or deficit for the period.

- Combined with the opening balance, leads to deriving the closing balance.

- It becomes opening balance for the next period.

Question 2. What is EOQ? How it is calculated?

Answer. Economic Order Quantity (EOQ) is an important tool in the purchase of raw materials and storage of finished goods. Generally to determine the optimal order of quantity of a particular item of inventory to be purchased at a particular time, which gives maximum economy to an entrepreneur, is called “EOQ”.

It is calculated on the basis of the given formula:

\(EOQ=\sqrt { 2DP/C } \)

Where D= the annual usage (or demand) of the item in units P = the cost of place on order C = inventory carrying cost per unit (This may be derived by multiplying the unit price of the item by carrying cost expressed as % of the unit price.)

The above formula minimizes the total cost of managing inventory consisting of ordering cost and carrying cost of inventory. The two costs are inversely related, when the one increases the : other decreases with the change in the purchase quantity of inventory. It is a balance between the two opposing cost-carrying cost and order processing cost, can be achieved by computing the economic order quantity.

Question 3. Give the formula of EOQ and write down its assumptions.

Answer. \(EOQ=\sqrt { 2DP/C } \)

where D = the annual usage (or demand)

of the item in units

P = the cost of place on order

C = annual carrying cost per unit

The above formula is based on following assumptions:

- Ordering cost is constant i.e. it is independent of size of the order.

- The cost of carrying additional inventory is constant.

- There are no quantity and discounts available.

- The consumption is in a steady rate.

Question 4. Why is inventory control essential for an enterprise?

Answer. Inventory control is essential for an enterprise because:

- It ensures the availability of materials in the production process whenever it is needed.

- To ensure efficient and effective utilization of raw materials.

- It helps in removing all bottlenecks.

- To ensures prompt and regular delivery of materials to consumers.

- To examine quantity discount for large and lump sum order to stabilize the fluctuation of demand side.

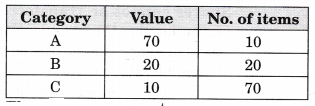

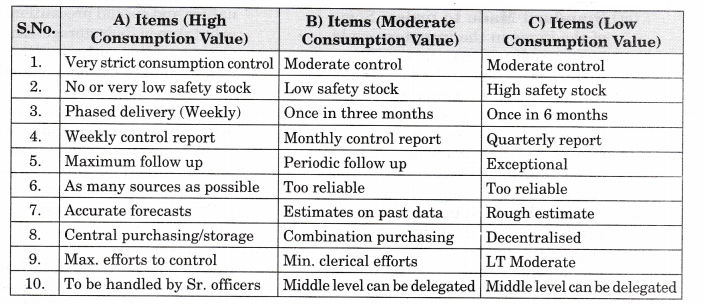

Question 5. Explain ABC Analysis of Inventory Control.

Or

Which items of inventory claim bulk of the values?

Answer. A firm maintains several types of inventories. To control them properly the firm adopts a selective approach which is called ABC Analysis. In this the firm classifies all items according to values so that the most valuable items may be paid highly, more attention is given regarding their safety and care as compared to other items. It has been observed that out of a long list of inventory,

A category list are small in number say 5-10 per cent of the total value but they are quite valuable of total value. The value being 70-75 per cent of the total value of stocks.

B category is in between A and C categories having 15 to 20 per cent of the number of items and 15 to 20% of the total value.

C category items are 70-75% in numbers but carrying little value ranging from 5-10%.

We can see following categorization:

The above three categories vary from product to product and organization to organization. Great care and control is to be exercised on items of “A” list, as any loss or breakage or wastage of any item of this list may prove to be very costly, proper care is to be taken on “B” list items and comparative list control is needed for “C” list items.

Question 6. What do you mean by Break Even Point? Explain its importance.

Answer. Break even point is a neutral point at which the company neither makes a profit nor suffers a loss. Calculating the break¬even point is a powerful quantitative tool for managers.

In its simplest form, break even analysis provides insight into whether or not revenue from a product or service has the ability to cover the relevant costs of production of that product or service. Entrepreneurs can use this information in making a wide range of business decisions, including setting prices, preparing competitive bids, and applying for loans. It also helps in profit planning and goal setting.

At the break even level,

Total Revenue = Total Expenses The formula for calculating break even level is:

Break Even Volume=Fixed cost/Gross margin

Gross Margin Per Unit = Unit Price (Selling price) – Marginal Cost (Variable cost)

Contribution per unit = Selling price per unit – Variable cost per unit Or

Contribution Ratio = Selling price – Marginal cost

Marginal Cost = Total variable cost Or = Total cost — Fixed cost

Or = Direct material+Direct

labour + Direct expenses + Variable overhead

The ‘Break-even Point’ is that volume of sales at which total revenue is equal to total costs, with zero profit. ‘Break-even point’ is a situation where the firm is neither in profit nor loss. In other words, this is a ‘no-profit, no-loss situation’. When the organisation is not able to earn profits, the best alternative for the firm is, at least, not to incur loss. So, organisation would like to know at what level of production and sales, the organisation would be able to achieve no-loss, no-profit situation. This is the greatest contribution of ‘Break-even Point’.

Question 7. State the advantages of‘cost plus’ method of pricing. [All India 2015]

Answer. Advantages of Cost Plus method of pricing:

- Easy: This method of pricing is very simple method. It can easily be used for determining the price.

- Flexible: Any changes in the cost of production or the margin of profit change the price in the same direction. It automatically gets adjusted to the change.

- Visible profit margin: Profit margin is not to be calculated. It is already fixed. Thus by multiplying the profit per unit with the volume of the product, the total profit can be determined.

- Increases efficiency: Any upward rise in cost is easily visible. This provides an idea to the entrepreneur to adjust his production for keeping the cost as low as possible.

- Less calculation: Comparatively less calculations are involved. Which makes the implementation of this method simple,

- Easy implementation: This method can easily be implemented because of its simplicity to understand and easy calculations.

Question 8. Explain the following features of a cooperative society:[CBSE Sample Paper 2016]

- Democratic management

- Capital and return thereon

- Distribution of surplus

Answer. Features of Co-operative societies:

- Democratic management: The management of a co-operative organisation is vested in the hands of the managing committee elected by the members on the basis of ’one member-one vote’. Democracy is, thus, the keynote of the management of a co-operative society.

- Capital and return thereon:The capital is procured from its members in the form of share capital. A member can subscribe subject to a maximum of 10% of the total share capital or Rs 1,000 whichever is higher. Shares cannot be transferred but surrendered to the organisation. The rate of dividends paid to the members/ shareholders is restricted to 9% as per the Co-operative Societies Act, 1912.

- Distribution of surplus: After giving dividends to the members, the surplus of profits, if any, is distributed among the members on the basis of goods purchased by each member from the society.

IV. VERY LONG ANSWER TYPE QUESTIONS

Question 1. Differentiate between cash flow projection and cash flow statement.

Answer.

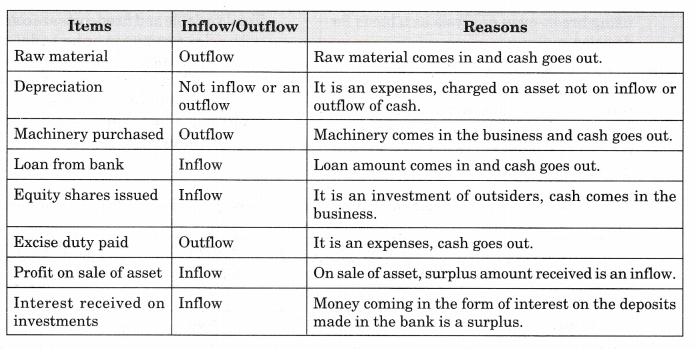

Question 2. Identify the following items as inflow/outflow. Also give reasons for your choice.

(i) Raw material, (ii) Depreciation, (iii) Machinery purchased, (iv) Loan from bank,

(v) Equity shares issued (vi) Excise duty paid, (vii) Profit on sale of asset, (viii) Interest received on investments

Answer.

Question 3. Why there is a need for cash flow projection?

Answer. The following are the need of cash flow projection:

- Every business must want to manage its affairs in a very efficient manner.

- It means it must pay its suppliers as per agreed terms, pay the employees their wages on stipulated dates, pay government levies, etc. as per rules, procure services and pay for the same, pay utility bills and rent etc., on time.

- It must collect what is due to it also in a timely manner and should strive to sell more so it can collect more.

- Very often, when business is expanding, your outflows can be more than in your inflows. This is so because there is always a lag between your spending (on raw materials, labour, etc.) and your receiving the sales revenue.

- Receipt of sales revenue may be delayed because you might have given credit or you have produced ahead of the sales (to cater to the high demand during festive season) and are temporarily holding finished goods stock.

- In such situations, you should be equipped with sufficient information to be able to arrange for needed funds.

- The nature of any business is uncertainty. You base your calculations on certain (hopefully realistic) assumptions.

- It plans the funds required using these assumptions. ‘

- However, your actual performance, say of sales, could be higher or lower than your plan. It will rarely be exactly per plan.

- Or your collection from credit customers has lagged and you are running short of funds. There could be many other reasons as to why your well laid out funding plan has gone for a loss,

- To avoid such situations and be on top of things, reviewing your projections periodically and recasting the future based on the current status (and not assumptions of the past) and what is likely to happen in the near future is very crucial.

- Cash flow projections is not a static document. It must be used as a dynamic tool.

V. HIGHER ORDER THINKING SKILLS

Question 1. Explain why break-even analysis is of reduced value to a multi-product firm? Analyse the factors that any business should take into consideration before using break-even analysis as a basis for decision making.

Answer. Break -even analysis is a technique widely used in the manufacturing unit by the production manager It is based on categorising production costs between two types of cost:

- Fixed cost

- Variable cost

From the above two examples we can understand that unit price of single product is comparatively higher than the unit price of a multiple product.

Businesses dealing with multiple products must reduce all the selling prices down to one selling price and bring down to one variable cost. This is accomplished by calculating a weighted average selling price and a weighted average product cost (variable cost). Further, when the weighted average selling price and weighted average variable cost are calculated, only then can a business, selling multiple products, determine their break-even point. Moreover, businesses selling multiple products will determine their break-even point using the following Break Even formula:

Break-even point =Fixed Costs/Weighted Average Selling Price – Weighted Average Variable Costs

As you can see, the break-even point formula for businesses selling multiple products is similar to the formula used by businesses selling a single product. The only difference is the term “weighted average” placed in front of the selling price and variable cost. It is important to understand the concept of weighted averages.

- Calculating the break-even point (through break-even analysis) can provide a simple, yet powerful quantitative tool for managers.

- The analysis provides insight into whether or not revenue from a product or service has the ability to cover the relevant costs of production of that product or service.

- Entrepreneurs can use this information in making a wide range of business decisions, including setting prices, preparing competitive bids, and applying for loans.

- It also helps in profit planning and goal setting.

Question 2. Explain the factors determining the working capital requirements.

Answer. Following factors determine the working capital requirements:

- Turn over: Higher is the sales turn over, lower is the requirement of working capital. The revenue is obtained from the current assets. On the other hand, lower is the sales turn over; higher is the requirement of working capital.

- Tax liability: Increase in the tax liability increases the requirement of working capital and decrease in the tax liability of the enterprise decreases the need of working capital.

- Size of enterprise: Larger is the size of enterprise; larger is the requirement of working capital. On the contrary, smaller is the size of enterprise; smaller is the requirement of working capital.

- Nature of the enterprise: Requirement of working capital is different type of enterprises. Restaurants, hotels, etc. have less working capital requirements due to cash sales. Enterprise producing heavy machines needs more working capital, as their operating cycle is longer.

(a) Operating cycle: Longer is the length of operating cycle larger is the requirement of working capital. This is due to the fact that more money is needed for making stocks, purchasing raw materials, etc. - Stock of inventory: If the enterprise prefers to make a larger stock of finished, semi-finished goods and raw materials, the requirement of working capital also matters. On the other hand, lesser is the stock of such materials, lesser is the requirement of working capital.

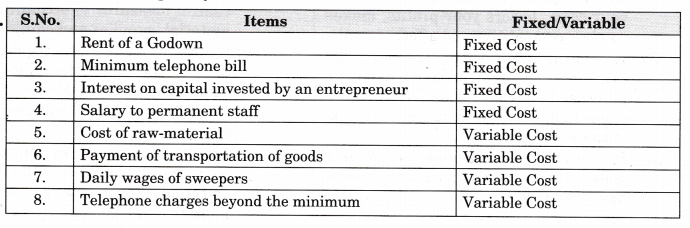

Question 3. Classify the following into fixed cost and variable cost:

(i) Rent of a Godown

(ii) Minimum telephone bill

(iii) Interest on capital invested by an entrepreneur

(iv) Salary to permanent staff

(v) Cost of raw-material, payment of transportation of goods.

(vi) Daily wages of sweepers

(vii) Telephone charges beyond the minimum.

Answer.

Question 4. State whether the following require small or large working capital. Answer should be supported by a valid reason:

(i) Selling ice-creams

(ii) Following a liberal credit policy

(iii) Dealing in stainless steel wares

(iv) Using capital intensive technology

Answer.

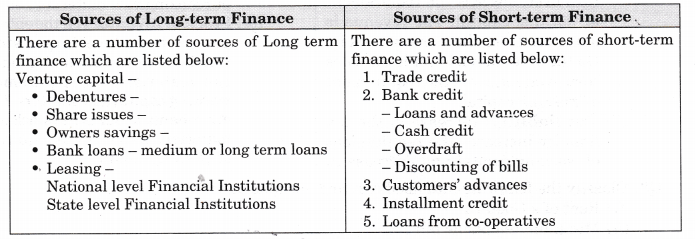

Question 5. On the basis of duration, classify the sources of finance.

Answer. Sources of finances can be classified on the basis of duration:

VI. VALUE BASED QUESTIONS

Question 1. How does pilferage of material affect the enterprise and entrepreneur?

Answer. Pilferage of material means – theft. In any enterprises or a business theft raises your costs, lowers your profits, makes you less competitive and affects morale.

Question 2. How can an entrepreneur or an enterprise can take preventive measures to reduce pilferage in an enterprise? What values can lead to a successful implementation of these measures?

Answer. In many enterprises/organisations generally most of employees are honest and disapprove of theft, pilferage of materials and resources in many organisations. But every enterprise must keep some strategies for prevention of pilferage within your company could include:

- Install adequate inventory and control measures to account for all material, supplies and equipment.

- One control method is the requirement, register and signing for all tools and equipment to be issued by individuals.

- Identify all tools and equipment by some mark or code.

- Conduct a meeting in the form of workshop to convince and educate the employees that they have much more to lose than gain by stealing.

- Make them understand and realize all employees that pilferage is morally wrong no matter how insignificant the value of the item taken.

- Demand that supervisory personnel set a proper example and maintain a desirable moral climate for all employees.

- In extreme situations, propose spot searches of employees and vehicles leaving the installation at unannounced times and places. Publicize widely.

- Impress upon all employees that they have a responsibility to report any loss to proper authorities.

- Value Points:

(a)Spirit of enquiry

(b) Discipline

(c) Sincerity

(d) Unwillingness to hurt by employer

(e) Duty and loyalty to duty.

Question 3. How cash flow projections will be helpful for an entrepreneur? What values can lead to a successful implementation of these programmes? (Value Points)

Answer.

- For an entrepreneur it is an important tool for cash management.

- He will be able to verify when his outlays/outflows are too high or when you might want to arrange short term investments to deal with a cash surplus.

- A cash flow projection will give a much better idea of how much capital investment a business idea needs.

- Measurement is essential to analyse performance of any business. Given below are some businesses and items being sold/serviced by them.

- Value Points:

(a) Self- control

(b) Duty and loyalty to duty

(c) Discipline id) Self-support

(e) To protect national property

(f) Concentration.

Question 4. Explain the main objectives of financial management which is helpful to the enterprise? (Give four value points)

Answer. Financial management is needed because of the following:

- To protect against unforeseen circumstances: Entrepreneur minimizes the risks by making a estimate of risks. For this purpose, he prefers to manage his money (finance) by keeping in mind its requirement in the future.

- To maximise profit: By managing the finance effectively, the entrepreneur tries to maximize his profit. Finance like other resources is available in limited quantity. Efficient utilization of finance is the only way for profit maximization.

- To acquire assets: Any type of asset whether tangible or intangible, need finance for acquiring them. As the enterprise grows, develops or diversifies, the requirement of finance also increases. Thus more is the finance available, more are the chances of acquiring new assets. Moreover from the present income the provision is to make for meeting future obligations. This needs proper management of finance.

- To maximise wealth: As the profit increases the wealth of the entrepreneur and the enterprise both are maximized. Goal of wealth maximization is realized by entrepreneur by making optimum utilization of resources, by maintaining the faith of the shares, by properly utilizing the undistributed profit etc.

- To ensure ready availability of funds: The flow of funds must take place as and when needed. At any point of time the shortage of funds is undesirable for the growth of enterprise.

- Value points:

(a) Proper utilization of time

(b) Universal

(c) Awareness of responsibility of others and employees

(d) Sincerity

(e) Team work and team spirit.

Question 5. Explain the benefits of budgeting. Give some value points.

Answer.

- For start up entrepreneurs, a budget is like a road map that can help them set goals and assess the validity of their business concept.

- For established small businesses, a budget can be used to take the pulse of the business, determining how the business is performing through the years, and helping identify possible future investments.

- By regularly consulting a budget, business leaders can compare actual figures and catch potential business shortfalls or other problems early. Budgets can also be instrumental in winning over investors, convincing banks your business is a good loan risk, or bringing on new partners or customers.

- The single-most potential benefit of formal budgeting lies in ensuring that responsible managers take time each year (and then at fixed intervals throughout the year) in thinking about their operation by looking at all of its aspects. Budgeting creates a comprehensive picture of the future and makes both opportunities and barriers conscious. This foreknowledge then helps guide day-to-day activities.

(a) Value Points:

(a) Regularity

(b) Positive performance

(c) Responsibility of managers and others

(d) Feasibility

(e) Deal with other problems and find solutions to it.

Question 6. Draw a diagram of an operating cycle or cash conversion cycle for large scale manufacturing business (in Detail). And explain how it is important for business (positive and adverse effects).

Answer. Positive Effects:

- Working capital is a life-blood of manufacturing unit. Its working capital financing can eliminate.

- Any gap between cash flowing into operations and cash flowing out.

- An adequate supply of raw material for smooth functioning of the process.

- Cash to meet the wage bill.

- Ability to grant credit facility to customer.

Adverse Effects:

- Due to inadequate funds. Growth of a firm may stop and it will become difficult for the firm to undertake important projects.

- Attractive credit opportunity may have to be lost due to paucity of working capital.

- It will be very difficult for meeting day-to-day expenses.

- Sometimes even fixed assets may not be efficiently utilized, it may affect low rate of return on investment in the working process.

- Firm may loose its reputation when sometimes not able to meet short term obligations.

Effects of Excess Working Capital:

- It may result in unnecessary accumulation of stock of raw materials and finished goods, leads to mishandling, waste, theft, value may depreciate.

- It shows managerial inefficiency.

- It may lead for making speculative profits.

- Undue incentive to adopt liberal credit policy.

Value Points:

- Regularity

- Positive performance

- Responsibility of managers and others

- Feasibility

- Social awareness

- Proper and maximum utilization of resources

- National awareness

- Self-discipline

- Concentration and social justice.

Question 7. In the following cases (statements) identify the type of budgets related to it:

- It always estimates of future sales, often broken down into both units and currency.

- It estimates the various costs involved with manufacturing those units, including labour and material.

- It is used to determine an organization’s long term investments.

- It also estimates the investment for research and development.

- It estimates the funds for promotion and advertising.

- It shows a cost estimated/associated and is used to establish a particular company project.

- An estimate of the number of units that must be manufactured to meet the sales goals.

- A budget which details the amount of cash you collect and pay out.

- This is generally tallied on a monthly basis, but some businesses tabulate this weekly.

- It helps you figure out how much money you need to put in place new equipment or procedures to launch new products or increase production or services.

- It estimates the value of capital purchases you need for your business to grow and increase revenues.

Answer.

- Sales budget

- Production budget

- Capital budget

- Capital budget

- Marketing budget

- Project budget

- Production budget

- Cash flow budget

- Cash flow budget

- Capital budget

- Capital budget

Question 8. Explain the concept of ABC Analysis.

Answer. The ABC approach states that a company should rate items from A to C, basing its ratings on the following rules:

- A-items are goods which annual consumption value is the highest; the top 70-80% of the annual consumption value of the company typically accounts for only 10-20% of total inventory items.

- B-items are the inter class items, with a medium consumption value; those 15-25% of annual consumption value typically accounts for 30% of total inventory items.

- C-items are, on the contrary, items with the lowest consumption value; the lower 5% of the annual consumption value typically accounts for 50% of total inventory items.

Through this categorization, the supply manager can identify inventory which is more important and more profitable, and separate them from the rest of the items, especially those that are numerous but not that profitable.

Steps involved in ABC Analysis:

- Find out the unit cost and the usage of each material over a given period.

- For each item calculate the total cost = Annual demand x Item cost per unit

- Arrange all items in a progressively decreasing order of the cost (descending value).

- Calculate and tabulate the cumulative total cost.

- Calculate percentage on total inventory in value and in number.

- Compute the individual items as a percentage of the total number of items

- Tabulate.

Question 9. Explain the concepts of working capital with the help of an example.

Answer. Concept of Working Capital: Generally, there are two concepts of working capital i.e. gross concept and net concept.

- Gross Concept of Working Capital: According to gross concept, working capital refers to all the current assets and represents the amount of funds invested in current assets.

(a) Thus, gross working capital is the capital invested in current assets. Current assets are those

assets which can be converted into cash within the short-time period, (say for 12 months )

(b) Gross working capital = Total current assets

Gross working capital refers to the firm’s investment in current assets. Gross working capital represents total of current assets which includes cash in hand, cash at bank, inventory, prepaid expenses, bills receivable, etc. - Net Concept of Working Capital: According to the net concept, working capital is the excess of current assets over current liabilities. In other words, the difference between current assets and current liabilities is called net working capital.

Net Working Capital = Current Assets – Current liabilities Net working capital is the difference of current assets and current liabilities.

(a) Gross Working Capital = Total Current Assets

(b) Net Working Capital/Funds/Net Current Assets = Current Assets — Current Liabilities

Example: Working capital of Raja and Co. has the following items in its Balance Sheet: Stock – 50,000: Trade creditors — 32,000; Debtors – 75000; Cash – 1,00000 Dividend payable – 50,000; Tax – 44,000; Short term loan — 61,000; Short term investments – 76,000. Calculate gross and net working capital.

Total Current Assets = Debtors + Stock + Cash + Short term investment = (Rs75000 + Rs 50,000 + Rs 1,00000 + Rs 76,000)

= Rs 3,01,000.

Total Current Liabilities =Sundry Creditors + Dividend Payable + Tax + Short Term loan = Rs 32,000 + Rs 50,000 + Rs 44,000 + Rs 61,000 = Rs 1,87,000.

Gross Working Capital = Total Current Assets = Rs 3,01,000 Net Working Capital = Total Current Assets – Total Current Liabilities = Rs 3,01,000 – Rs 1,87,000 = Rs 1,14,000 Gross Working Capital = Rs3,01,000 Net Working Assets = Rs 1,14,000.

Question 10. Enumerate the suggested policy guidelines for A, B and C classes of items.

Answer. The table given below explains the policy guidelines for A, B and C classes of items:

ABC (Always Better Control) analysis can help you control your inventory better.

Question 11. “For a good inventory control system, we need to take care of both physical and fiscal aspects.” Explain the nature of items that make up the inventory.

Answer. For a good inventory control system, we need to take care of both physical and fiscal aspects. But before we deal with those two, let us understand the nature of items that make up the inventory.

- Stock Keeping Unit (SKU) Code: Each and every item in the inventory is to be identified with a unique code which signifies certain aspects of the item.

It can be colour, size, weight or any other characteristic that is of importance in its use. The SKU code can be a combination of alpha and numeric.

SKU is the very basic unit for data collection and further manipulation for deriving meaningful statistics and decision-making. Bar Codes and RFID (Radio Frequency Identification) tags ‘ are used in tracking etc. using SKU. - Motley crowd:

(a) We always refer to inventory in one monetary value in the accounting statement, behind it are myriad numbers of SKUs – that can be classified as Raw Materials, Packing Materials, Spare Parts, Semi Finished Goods (or WIP – Work In Progress), Finished Goods, Consumables, etc.

(b) The SKU code should definitely help us identify which class the item belongs but not much else. The treatment for each class will have to be different, keeping in mind some of the factors identified here. - Space: Space requirement for all items will not be identical; neither will it have proportionate relationship with the cost of the item. There can be many bulky items with low value (For example, straw for use in paper mill) as well as high value items with low volume (For example, Diamonds).

- Value: Not all SKUs have same value.

- Lead time:

(a) Lead time to manufacture or procure an item depends on many factors. Combined effect of these factors — like standard or special raw material, processing time, scheduling of machines, distance between source and user point etc. – makes up the lead time for an item.

(b) It is not always the same for a given item; variability in different factors contributing to the total lead time can make the lead time vary. - Standard Made to order: Some of the items in the inventory could be commodity items – no significant differentiation and hence easy to substitute, or many suppliers produce to same specifications and hence easy to choose from.

(a) Others may be specifically made to order and hence possibly limited sources to order from. - Seasonality of supply: If the item is an agricultural product (grains, vegetables, fruits, etc.), the supply would be seasonal. This can play a role in designing the inventory control system.

- Demand neither uniform nor predictable:

(a) Demand for an item could be seasonal — weather, festival seasons, events, school opening, etc. can play a significant part in this.

(b) In some cases it is easy to forecast-raw material for items produced to order; but in others not so easy – requirement of a spare part. - Shelf life:

(a) Items like vegetables, fruits, flowers and fish are perishable in nature. This calls for special storage conditions and equipments – cold storage, freezers, etc. These, have financial implications.

(b) Some of the manufactured food or medicinal products have expiry dates— beyond which they are not fit for consumption. This imposes certain constraints on inventory management. - Safety aspects:

(a) Some of the items are hazardous in nature and special precautions have to be taken in their storage. Examples are — gasoline, other combustible items, some hazardous chemicals, etc.

(b) In a factory manufacturing safety matches, phosphorous and potassium chlorate are not stored in the same or even adjoining areas, for fear of accidental mix up. In fact, even their path of delivery to the respective end use points do not cross. - Obsolescence:

(a) Due to advancement in technology, certain items may not be used and their demand drops off. These are the various characteristics of SKUs that have to be kept in mind while designing inventory control systems – one size will not fit all.

(b) Different (rules and guidelines) will have to be different for raw materials, consumables, spare parts, packing materials, etc.

Question 12. Define budgetary control. State how “budgetary control” helps an entrepreneur?

Answer. Budgetary control is a technique of managerial control in which all operations are planned in advance. In the form of budget actual performance is compared with standard performance.

It also helps to achieve the organizational objective of an enterprises.

- Provides a source of motivation to employees and employers.

- It helps in optimum utilization of resources.

- It also helps to maintain the coordination among all the departments.

NCERT SolutionsHistoryPolitical ScienceSociologyPsychologyHumanities